| Broker | Offer | Minimum Deposit | Trade Now |

|---|---|---|---|

|

|

Assets: 300+

Min. Trade: $1 Payout: 100% Payout within 3 days |

$10

|

Trade Now |

|

|

Assets: 300+

Min. Trade: $1 Payout: 100% Payout within 3 days |

$10

|

Trade Now |

|

|

Assets: 300+

Min. Trade: $1 Payout: 100% Payout within 3 days |

$10

|

Trade Now |

|

|

Assets: 300+

Min. Trade: $1 Payout: 100% Payout within 3 days |

$10

|

Trade Now |

The SWIFT system is considered a key pillar of international financial communication today. It is a network created to allow banks worldwide to exchange financial information securely, quickly, and in a unified standard. This includes money transfers, transaction status notifications, and the transmission of various payment and trading instructions. Many banking customers often search for a swift code when preparing to transfer money abroad for various purposes, such as paying for goods, transferring tuition fees, sending personal funds, or conducting business between two countries. Understanding this system correctly is therefore highly beneficial, especially for those who need to use swift codes for all banks, to ensure that their cross-border transactions proceed without errors or delays.

History of the SWIFT system and its role in Thailand

The SWIFT system was established in 1973 by a group of more than 200 European banks that recognized that traditional financial messaging methods, such as telex or fax, carried high risks, lacked common standards, and were insufficient to support the growth of international transactions. With the creation of SWIFT, the system was designed to serve as a secure and globally standardized tool for financial communication.

Over time, the SWIFT network expanded rapidly, covering more than 200 countries and involving over 11,000 financial institutions worldwide, including Thailand, which officially joined in the early 1980s. Thailand’s participation helped raise standards of security and reliability in international transactions, especially during a period of continuous growth in global trade and foreign investment.

All major commercial banks in Thailand, such as Krung Thai Bank, Siam Commercial Bank, Bangkok Bank, and Kasikornbank, use this system as a core part of their financial data transmission, ranging from small personal transactions to large-scale corporate or multinational transactions. As a result, SWIFT has become an indispensable financial infrastructure for Thailand in the modern financial world.

The meaning of a SWIFT Code and basic operations

A SWIFT Code, commonly referred to in Thailand as “swift code,” is a code designed to clearly identify banks or financial institutions in each country. It can be compared to a financial address that global systems use as a reference. When a sender needs to conduct an international transfer, this code is essential for the system to determine which bank, which branch, and which country the funds should be sent to, helping reduce errors and increase accuracy in cross-border transfers.

The process begins when the sender enters the swift code into the transfer form. The information is then encrypted and sent through the SWIFT network to the destination bank in a standardized message format, which includes the transfer amount, sender and recipient details, currency, and other reference information. The receiving bank then verifies the data before executing the actual debit and credit process. This data-receipt stage takes only a few minutes, making international transfers smooth, accurate, and highly secure.

SWIFT/BIC codes of Thai banks

| Bank / Institution | SWIFT / BIC Code | City |

|---|---|---|

| Bangkok Bank Public Company Limited | BKKBTHBK (branch code may be added, e.g., XXX) | Bangkok |

| Bank of Ayudhya Public Company Limited | AYUDTHBK | Bangkok |

| Kasikornbank Public Company Limited | KASITHBK | Bangkok |

| Krung Thai Bank Public Company Limited | KRTHTHBK | Bangkok |

| Siam Commercial Bank (SCB) | SICOTHBK | Bangkok |

| TMBThanachart Bank Public Company Limited | TMBKTHBK | Bangkok |

| Government Savings Bank (GSB) | GSBATHBK | Bangkok |

| Standard Chartered Bank (Thai) | SCBLTHBX | Bangkok |

| Union Overseas Bank (UOB Thai) | UOBBTHBK or BKASTHBK | Bangkok |

| Bank for Agriculture and Agricultural Cooperatives | BAABTHBK | Bangkok |

| Bank of America, N.A. Bangkok | BOFATH2X or BOFATH2XTHA | Bangkok |

| Bank of China (Thai) PCL | BKCHTHBK | Bangkok |

| BNP Paribas Bangkok Branch | BNPATHBK | Bangkok |

| Deutsche Bank AG, Bangkok Branch | DEUTTHBK | Bangkok |

| Mega International Commercial Bank (ICBC) | ICBCTHBK | Bangkok |

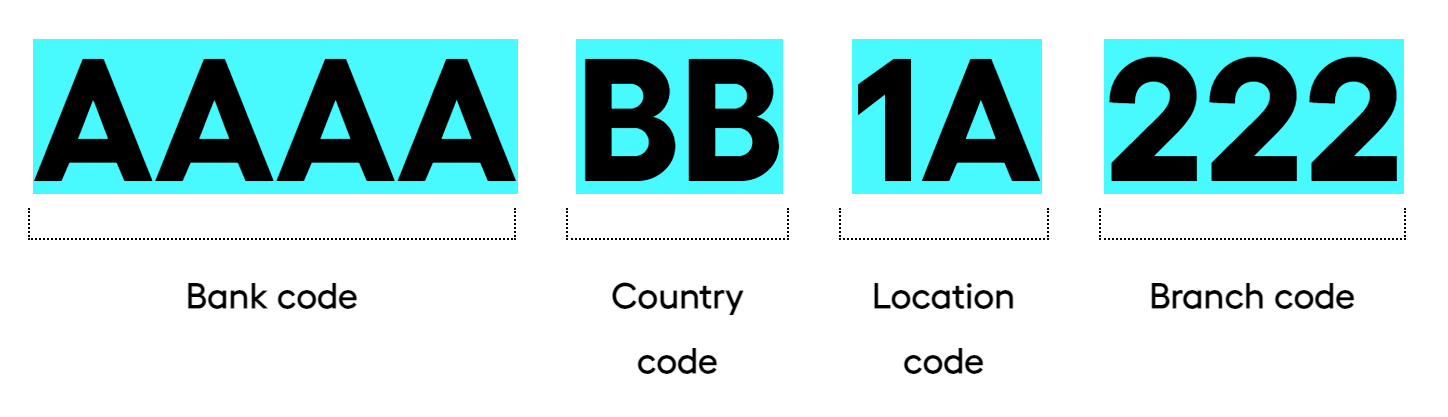

What does the structure of a SWIFT Code look like?

The structure of a swift code follows a standard format of 8–11 characters. Each letter and number in the code has a specific meaning, allowing the receiving bank to accurately identify which institution and which country the information relates to. The structure is as follows:

- First 4 characters: bank code, such as KASI for Kasikornbank

- Next 2 characters: country code, such as TH for Thailand

- Next 2 characters: city or bank location code

- Last 3 characters (if any): branch code, such as XXX for the main branch or head office

Users who understand this structure can more easily verify the accuracy of a code. For example, if a code is received from an overseas recipient, the sender can immediately check whether the country code is correct, helping reduce the risk of entering incorrect information. This is especially important when searching for and using swift codes for all banks, which may vary across different financial institutions.

Are SWIFT Codes the same for every branch?

Many banks choose to use a single SWIFT Code nationwide to make transactions as convenient as possible for users, often using XXX as the main branch code. However, some banks, particularly those with a high volume of international transactions, may assign specific codes to certain branches, such as branches that directly handle international trade operations or head office branches.

For example, the use of the Kasikornbank swift code is very common for transfers from overseas into Thailand. Many private businesses choose this bank for their transactions, making it especially important to verify the code correctly from the start. Users should always double-check the information to prevent transfer delays or transactions being rejected by the system.

What types of transactions require a SWIFT Code?

Many types of financial transactions require a swift code so that the banking system can accurately identify the routing of funds. Entering the complete and correct code is a fundamental step in ensuring that cross-border transactions are completed without issues. Transactions that require this code include:

- Transferring money from Thailand to overseas

This is the most common type of transfer, whether sending money to family members, paying medical expenses, or paying for goods in the destination country. The sender must use a swift code to ensure the funds are sent to the correct bank. - Receiving money from overseas into a Thai bank account

When receiving income or transfers from overseas partners, the recipient must provide the swift code of the Thai bank to the sender so that the funds are credited to the correct account without discrepancies. - International payment for goods

Import and export businesses rely heavily on this system, as transactions are often high in value. Having verified swift codes for all banks helps reduce the risk of payments being sent to the wrong financial institution. - Intercompany transactions

Multinational companies or organizations with branches in multiple countries use SWIFT transfers to securely move funds between headquarters and subsidiaries. - Transfers between accounts owned by the same person in different countries

Even if the accounts belong to the same owner, if the banks are in different countries, a swift code is still required to ensure proper system linkage. - Payment of tuition fees, medical expenses, or accommodation costs abroad

These are common transactions for students and international travelers. Timely and accurate transfers affect enrollment and access to medical services, making the correct use of a swift code especially important.

If these transactions do not include a complete swift code, or if even a single character is entered incorrectly, the receiving bank may be unable to process the information. This can result in delays, rejected transactions, or in some cases, additional fees charged to the sender by intermediary international systems.

How to find the SWIFT Code of Thai banks

Users can search for a swift code in several ways, depending on convenience and the preferred channel. Reliable sources include:

- Official bank websites

Every bank provides information about international transfers and clearly states its SWIFT Code. - Mobile banking applications

This is the most easily accessible channel for users and usually displays the code in the international transfer menu. - Bank statements

Some banks print the swift code on monthly statements to make it easier for users to check. - Bank-issued documents such as a Letter of Certification

These are used to confirm account details for international transactions. - Contacting the bank’s call center

This method is suitable for users who are unsure or making their first international transfer, allowing them to confirm details with confidence.

In addition, searching for swift codes for all banks directly through the SWIFT website provides the most up-to-date information, as the system is regularly updated and covers financial institutions worldwide.

Using bank websites or mobile apps to search

Using a banking application is considered the most convenient option because, in addition to displaying accurate information, it helps reduce the risk of data entry errors. Most apps offer an automatic search function for swift codes for all banks from SWIFT’s central database, ensuring that the entered code always matches the destination bank.

In some banks, when users select the destination country and account, the system immediately displays the correct code to prevent the use of outdated information. This significantly reduces the likelihood of transaction errors.

Using bank websites or mobile apps to search

Using a banking application is considered the most convenient option because, in addition to displaying accurate information, it helps reduce the risk of data entry errors. Most apps offer an automatic search function for swift codes for all banks from SWIFT’s central database, ensuring that the entered code always matches the destination bank.

In some banks, when users select the destination country and account, the system immediately displays the correct code to prevent the use of outdated information. This significantly reduces the likelihood of transaction errors.

Steps to prepare information before making an international transfer

Before initiating an international transfer, the sender must prepare the following information in full:

- Recipient’s full name

- Destination account number

- Bank name and country

- Address of the destination bank

- Purpose of the transfer

- Correct swift code

- Supporting documents such as invoices, proof of income, or business-related documents

This information is extremely important because the destination bank uses it to verify identity and confirm the accuracy of the incoming funds. If the information is incomplete, the transfer may be delayed or rejected by international security screening systems.

What you should know about SWIFT before getting started

Although using a swift code is not complicated, there are important details users should understand to avoid issues such as high fees or long processing times. Users should always verify all information before confirming a transaction.

Fees for international transfers

Fees may include several components:

- Sender bank service fees

- SWIFT service fees

- Intermediary bank fees

- Receiving bank fees

- Currency conversion fees

Senders should check the fee-bearing option, such as OUR, SHA, or BEN, to choose the most appropriate option for their transaction type and budget.

Processing time for receiving funds

In general, recipients receive funds within 1–5 business days, depending on the destination country, the number of intermediary banks involved, and the completeness of the information provided. If the swift code is entered incorrectly or the information is incomplete, the transfer may be delayed or returned, resulting in additional time required for correction.

Documents required for international transfers

Users are required to prepare:

- National ID card or passport

- Transfer request form

- Documents confirming the purpose of the transfer, such as invoices, enrollment documents, or business-related paperwork

- Proof of income or financial contracts (if required)

For some countries, such as the United States or many European nations, financial regulations are particularly strict. Users should therefore check all conditions before making a transfer each time.

Differences between SWIFT Code and IBAN (not used in Thailand but useful to know)

Many customers are often confused about whether swift codes and IBAN serve the same function. While both are used in international transfer processes, they differ significantly in practice. A swift code is used to identify a financial institution, such as the bank or branch to which funds should be sent, specifying the country, city, and destination entity. IBAN (International Bank Account Number), on the other hand, is longer and more complex because it is designed to identify the destination bank account in much greater detail, including the account number, branch, and the country where the account is held.

The purpose of IBAN is to reduce errors caused by incorrect account number entry, particularly in Europe, where transfer standards are very strict. Thailand does not use IBAN for domestic transfers, so when sending money to Thailand, only a swift code is required. However, when transferring funds to Europe, the Middle East, or some Latin American countries, senders must provide both the IBAN and the swift code in full to allow the receiving bank to accurately verify the information. This is considered essential basic knowledge for anyone engaging in cross-border financial transactions before beginning actual use.

Advantages and disadvantages of the SWIFT system

The SWIFT system continues to be widely used around the world by banks, financial institutions, and business organizations, as it offers high stability and is recognized as one of the most secure infrastructures for financial messaging. However, the system also has certain limitations that users should be aware of and understand in advance in order to reduce risks when conducting transactions.

Key advantages of using a SWIFT Code

- High security through international-standard encryption

The SWIFT system uses modern encryption technologies that meet global standards, ensuring that financial data is strictly protected. - Supported by major banks in virtually every country worldwide

With a network covering more than 200 countries, almost all major banks use this system, making transactions highly reliable. - Suitable for large amounts and transactions requiring stability

Organizations often use this system for import, export, or international investment transfers because of its proven accuracy and reliability. - Ability to track transfer routes

Users can request information about the routing of transfer messages through their bank, which helps resolve issues in cases of delays or data errors. - More stable than alternative technologies in many countries

Despite the emergence of new digital transfer services, SWIFT remains the most trusted infrastructure for organizations and governments in many regions.

Latest SWIFT CODE updates for banks in Thailand

In Thailand, banks periodically update their swift codes to support internal infrastructure changes, such as office relocations, changes in branches responsible for international transactions, or updates in line with new international SWIFT standards. Users should therefore always verify the latest code before making a transaction, especially those who transfer money frequently, such as overseas workers, international students, or import–export businesses.

One of the most frequently searched codes is the Kasikornbank swift code, as this bank has a large customer base and plays a significant role in international fund transfers. Checking the official bank website is the safest method, as the information is updated directly from the central system and reduces the risk of using outdated codes.

Users who want to search for swift codes for all banks can check the official SWIFT website, the information center of the Bank of Thailand, or their own bank’s mobile application, which is currently the fastest and most convenient option. Preparing the correct code information helps ensure that transactions are processed smoothly, securely, and with minimal risk of errors.

You might also be interested in:

Binance Thailand Review

Withdrawing funds via Skrill to a bank account